As we get closer and closer to entering 2024, interest rates continue to be a leading topic of conversation in the real estate market. Will rates keep going up? Will rates come down? If so, when? There are many questions about how various factors affecting both the national and global economy will affect interest rates and in turn impact buying or selling a home.

In this blog, we will examine what we see in the upcoming horizon with interest rates and what our expectations are for 2024. We hope that reading this blog will help you become more informed about the current interest rate climate and in turn, provide you with useful takeaways that will help you better understand your personal real estate situation.

Whether you are looking into potentially purchasing a home in Silicon Valley in 2024 that will require financing, or if you are a seller keen on understanding how interest rate fluctuations affect the potential value of your home, this blog is for you.

LOOKING BACK

Before we jump into the future and theorize about what may be in store for us in 2024, let’s take a look back at some of the factors that have led us to where we are today in terms of interest rates. We seldom can predict the future if we cannot understand the past.

In the 2010s, a decade that followed one of the largest economic downturns in national history, interest rates stayed consistently low. Seeking to avoid another Great Recession, the Federal Reserve regularly supported friendly borrowing conditions, in hopes of spurring the economy forward. Average annual mortgage rates fluctuated between 4.69% and 3.65%. By 2019, the annual average was 3.94% and inflation was under 2%. Overall, in the 2010s, the Federal Funds Rate (the interest rate at which banks lend money to each other overnight) stayed close to zero with a slight rise towards the end of the decade.

As we all already know, 2020 changed everything. Adjusting on the fly in response to the Coronavirus Pandemic, the Federal Reserve dropped the Federal Funds Rate nearly to zero. For the first time, the 30-year fixed rate for a mortgage dropped below 3%. In an effort to keep the economy afloat an incredible amount of money was infused into the economy. Stimulus checks distributed to Americans began to drive inflation, which was expedited by supply-chain and production challenges that drove up the price of goods. Easy access to money meant that people were willing to spend, and real estate began to boom as mortgage rates stayed consistently low.

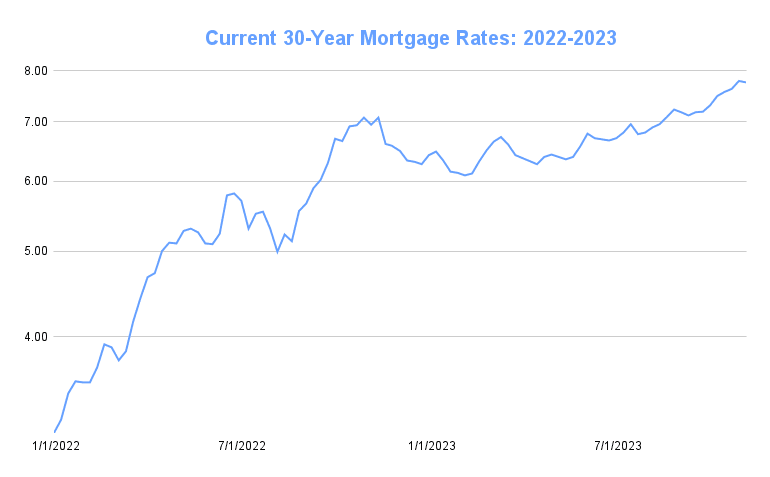

By early 2022, the Federal Reserve knew that it had to act—and fast. Beginning in March 2022, the Federal Reserve began raising interest rates. Between this first raise in March 2022 and May 2023, the Fed raised interest rates 10 consecutive times. This was a drastic action that the Fed felt was required to combat inflation that had reached a 40-year high.

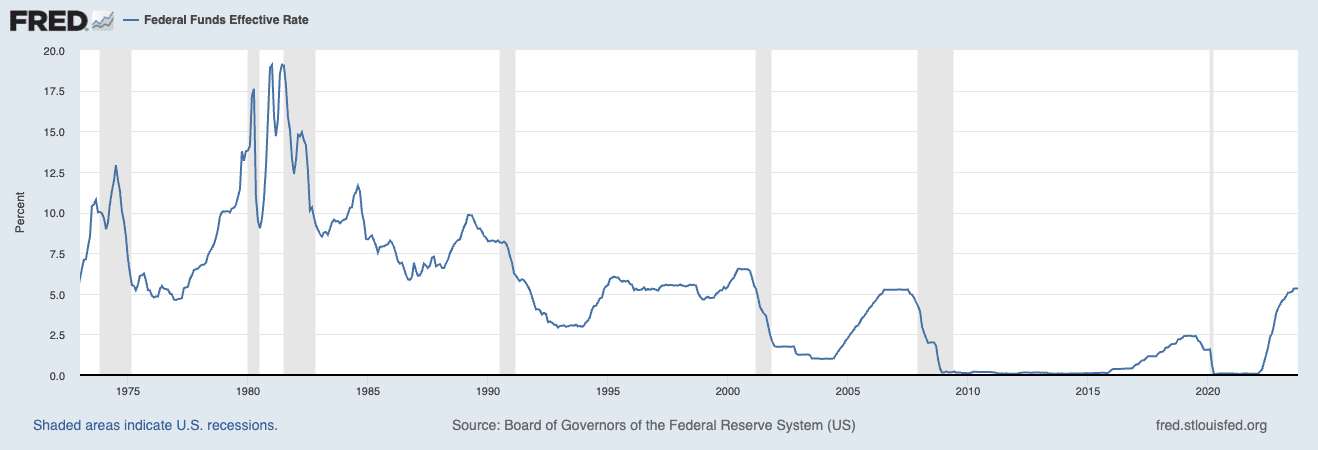

FEDERAL FUNDS RATE PAST 50 YEARS

Chart represents Federal Funds Effective Rate since January 1st, 1973. Source: Federal Reserve Bank of St. Louis | fred.stlouisfed.org/series/FEDFUNDS#

As a result of these measures, spending cooled. The Silicon Valley real estate market was hit hard and fast and rapidly rising interest rates meant that potential home buyers were now looking at significantly higher monthly payments for potential purchases. Sellers responding to these market conditions have often decided to take a “wait-and-see” approach. They are monitoring the interest rates closely hoping that any type of decrease will bring to the market a fresh and hungry wave of new potential buyers.

Optimism is present however, as the Federal Reserve has only raised rates once since May (in July), and inflation is now at a much lower rate around 3 or 4 percent, an incredible improvement over where it was just last year around historic inflation rates of 10 percent.

LOOKING FORWARD

As the Federal Funds Rate is no longer actively rising and inflation in our country is consistently going down, we are optimistic about interest rates in 2024.

Buyers and sellers who have never before seen mortgage interest rates of 7 or 8 percent likely will get some reprieve, and we do anticipate more movement in the market.

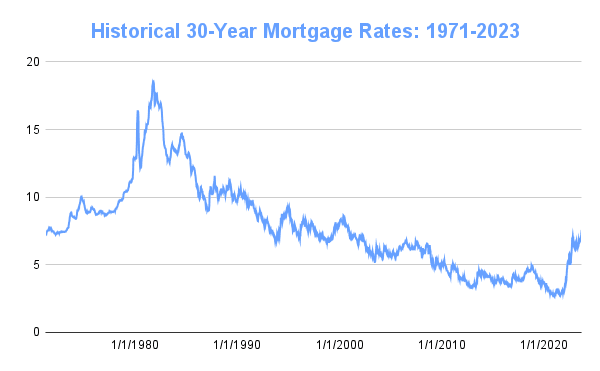

Chart represents weekly averages for a 30-year fixed-rate mortgage. Average for 1971-2023 as of November 9, 2023. Source: Freddie Mac PMMS. (c) TheMortgageReports.com

“Mortgage rates are plunging with the news of inflation calming. The interest rate rises should be over, and the Fed will have to consider cutting interest rates seriously,” said Chief Economist for the National Association of REALTORS® Lawrence Yun in his instant reaction article on November 14, 2023.

“In the meantime, the bond market is reacting as if the Fed will be cutting interest rates next year. Mortgage rates look to head towards 7% in a few months and into the 6% range by the spring of 2024,” also said Yun.

Sounds like everything is moving along well with economic indicators and interest rates should drop any day now right? Not so fast! What is important to consider is that even if the Federal Reserve reaches its inflation targets, that doesn’t guarantee that it will take drastic action and immediately begin dropping rates.

The commitment to a steady rate that we have seen from The Fed in the second half of 2023 suggests to us that if The Fed does begin to drop rates, it will be minimal and in slow increments.

“The fact is the committee is not thinking about rate cuts right now at all. We’re not talking about rate cuts,” Chair of the Federal Reserve Jerome Powell said during The Feds November 2023 meeting.

“We’re still very focused on the first question, which is ‘Have we achieved a stance of monetary policy that’s sufficiently restrictive to bring inflation down to 2% over time, sustainably?’ That is the question we’re focusing on,” added Powell.

Chart represents weekly averages for a 30-year fixed-rate mortgage. Average for 2022-23 as of November 9, 2023. Source: Freddie Mac PMMS. (c) TheMortgageReports.com

Basically, don’t expect The Fed to cut the rate in half just because inflation gets to where they want it. The Fed does not want to regress all the work that has been done to get the economy back in a stable place. They will likely not make knee-jerk reactions even with the pressure from politicians, the business community, and the general public.

Unless the economy slips into a prolonged recession, do not expect The Fed to make extensive interest rate cuts.

FINAL THOUGHTS

With inflation going down and the government not raising the Federal Funds Rate in months, we can confidently forecast that interest rates will go down in 2024. With interest rates going down, we should see mortgage rates go down as well. This should bring in a larger crop of potential buyers to the market which will in turn motivate additional sellers to put their homes up for sale. This should drive increased real estate sales volume in 2024 in comparison to 2023.

However, we do believe that any drops in interest rates will come at a reserved pace. Do not expect a repeat of 2020 & 2021 with mortgage rates hovering around 3 percent.

That COVID-impacted real estate market is long gone and current buyers and sellers need to face the reality that we are in a post-COVID market that has been hammered by inflation. Curtailing this inflation has been the priority of the Federal Reserve. Unless there is a serious economic recession, do not expect The Fed to make any drastic cuts.

Overall, however, we do expect a drop in overall national interest rates which will drive mortgage rates down in 2024. This will definitely have an impact on the market in terms of overall inventory.

A final thought for you—home prices will likely stay high even if interest rates do drop, as lower rates will attract more buyers, which will increase competition and raise prices due to increased demand.

“I don’t think any drop in interest rates will make housing more affordable for people looking to purchase a home,” says Sipho Simela, CEO and founder of Matrix Rental Solutions. “This is because supply will most likely get even tighter as more people start looking to buy due to lower interest rates.”

Whether it be Los Gatos luxury estates, San Jose neighborhoods, or Campbell single-family homes—if you are a homeowner in Silicon Valley, we anticipate that you will be able to sell your home for a premium in 2024.

Are you looking for the top Los Gatos REALTORS® at The Agency? Follow the Veeravalli Team for an exclusive look at Los Gatos, Cambrian, Campbell real estate and more.

About the Veeravalli Team

Ranked among the Top 1.5% Real Estate Agents nationwide according to the latest annual report by RealTrends, the Veeravalli Team is a husband-and-wife duo known for their data-driven approach and deep market expertise. With over 20 years of combined experience, they specialize in helping clients buy and sell homes across Blossom Valley, Almaden Valley, Cambrian, Los Gatos, and surrounding areas in Silicon Valley. As trusted relocation specialists, they bring precision, professionalism, and a personalized touch to every transaction, ensuring a smooth experience for both local and relocating clients alike.

VEERAVALLI TEAM

Ashwin Veeravalli

(408) 784-6595

LIC. #01914395

Aparna Veeravalli

(408) 887-0330

LIC. #01952626

The Agency Los Gatos